H-Spectrum - cyclical portrait of American stocks for the last 24

years

written

by Sergey Tarasov

H-Spectrum: how to do that

H-Spectrum stands for

"histogram based" spectrum. To get it, we start with calculating a

periodogram. Below is a sample of the periodogram. It represents the cyclical

activity, or, we can say, shows the most common cycles that can be found in American

stocks price charts since 2000 (i.e. for the last 24 years):

This is a very detailed chart;

it involves huge calculations. To get this sample, we have calculated

periodograms for 12 American stocks (Bartels-Tarasov algorithm was applied), on

different randomly chosen time intervals. By moving the LBC (learning

border cursor ), the data interval used for

calculations covers a period since the year 2000 till 2024.

Let us start calculating a

periodogram just for one stock. The program automatically has extracted the most

important cycles for its price chart; these are seen as peaks on the

periodogram. This is how a typical periodogram for one stock looks (JPM; LBC

set to April 2020):

Vertical stripes represent the

most significant cycles revealed by the periodogram; its peaks indicate the

cycles that accumulate more energy.

We can do the same for any

American stock. We can do that for all American stocks, one by one. As a

result, we get a huge list of cycles that were found for these stocks. We can

get a library of those cycles. We will see there that some cycles appear more

often than others. It could be a research project - looking at each cycle

separately and selecting those that are relevant for several stocks, groups of

stocks, etc. Finding a cycle/cycles that work for many

stocks sounds like a promising idea. However, it is too time consuming while

its outcome is unclear.

To get some confidence of our results we can display several periodograms

together to see what cycles appear more often. Here are four periodograms

displayed together; these are calculated for different stocks and LBC

positions:

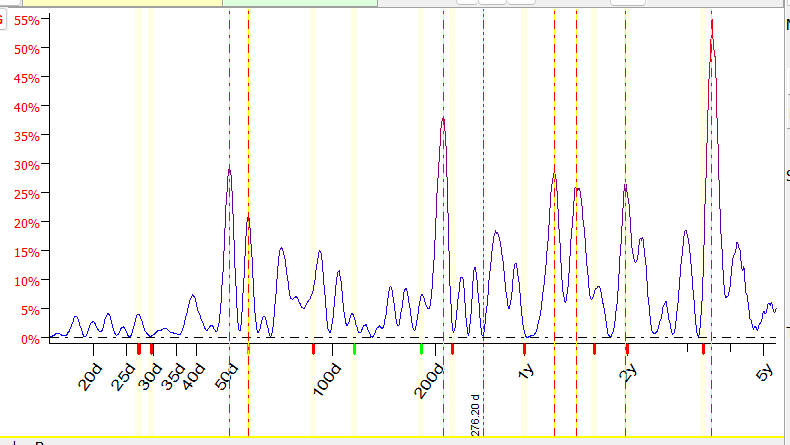

The red chart in the bottom

panel is a summary chart. It is called H-Spectrum. As you can see, it shows a peak around 2 years cycle; this peak

reflects the fact that this cycle is present in all these four periodograms.

Adding 4 more periodograms, we

get H-Spectrum based on 8 periodograms. It

reveals 95 different cycles. And you can see there two peaks now, two the most

common cycles for these 8 periodograms - 2 and 3-years cycles:

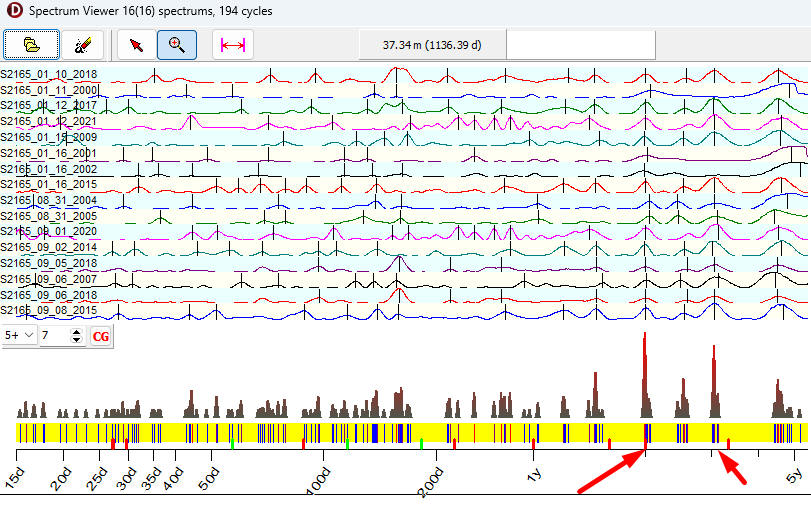

16 periodograms reveal 194

cycles; the final red chart looks even better:

To get the full picture, we

have analyzed 4695 periodograms (for different US stocks and different LBC

positions). These periodograms take into account 56K

cycles. The final histogram is based on 56K cycles; it looks very sufficient

from the statistical point of view:

It certainly shows some

clusters, some zones where cycles appear more often.

I was surprised to find a

3-years cycle as the most often appeared cycle, I expected to see there 40-42

months Kitchin inventory cycle that is revealed by classical cyclical analysis.

The Kitchin cycle is present there, it is also strong, though not so strong as

3-years cycle:

In the demonstrated approach we

applied a combination of classical cyclical analysis (by calculating

periodograms) and statistical analysis. As the result of this combination, we

have got a special type of Spectrum, H-Spectrum. It is a histogram that visualizes a frequency of the

appearance of different cycles. This is not a result of some activity of AI

(Artificial Intelligence, the software users often ask about that), this is a

kind of big data analysis or data mining.

As to my knowledge, we (Timing

Solution team) are the first who applied this approach. In 2017, while working

on stocks genome (see this article: https://www.timingsolution.com/TS/Articles/Genome/index.htm

), I tried to present the frequency of cyclical appearance as a histogram

chart. It is possible that someone else did that, too, though I have not seen

any referral to such approach among scientific papers that were available to me

at that time. The closest approach I was able to find is M.S. Bartlett and P.D.

Welch's method of averaged periodograms. There is a significant difference

there: we analyze histograms for extracted cycles while Bartlett/Welch are

focused on smoothing a set of periodograms.

H-Spectrum: H means Histogram

Soon after the introducing this

feature to Timing Solution community, H-Spectrum became one of the most used

tools of the Timing Solution software. I would like to explain in details how it works.

H-Spectrum = Histogram Spectrum

is, as it is assumed by its name, just a histogram, or the distribution of

cycles in regards to their periods.

You can easily visualize the

idea of a histogram. Imagine a set of bins. And a big bin with the balls of all

sorts and colors, like this one:

The balls in the big bin are a

mess. We can sort them, using those empty smaller bins. We put orange

basketballs into one bin, baseballs into another, foot balls into the third,

red, green, other ones - into other empty bin

accordingly. Now we see and we can say how many balls of each kind we have.

The same idea is for the cycles

that were extracted from the price charts. We put them into appropriate

"bins". Let say that the Spectrum module has revealed a cycle with a

period less than 10 days; we put this "ball" into the first bin (have

you noticed - I am not using "" for the bin, as it is a regular term

for an element of a histogram?). If the cycle's period is between 11-20 days,

we put the ball into the second bin. And so on.

Filling the bins, we process

all our periodograms/revealed cycles. The most loaded bins correspond to the

most common cycles, cycles that appear more often than others.

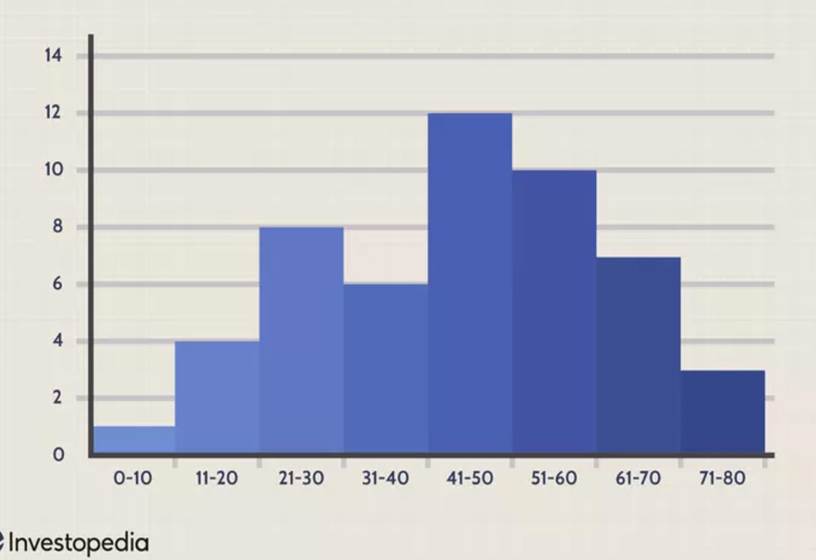

Usually a histogram is presented this way (this

image from Investopedia is included for illustration purposes

only; the original was applied for some other need):

Here the height of the first

bin (0-1) is 1; it means that only one cycle with a period no more than 10 days

has been found.

Cycles with periods 11-20 days

appear more often: 4 of these cycles have been found.

The most typical cycles are

41-50 days ; 12 cycles found, 12 balls in the bin.

Thus you can easily see more or less typical

cycles. The amplitude of H-Spectrum just shows how often some cycle appears, it tells you nothing about the amplitude of these

cycles.

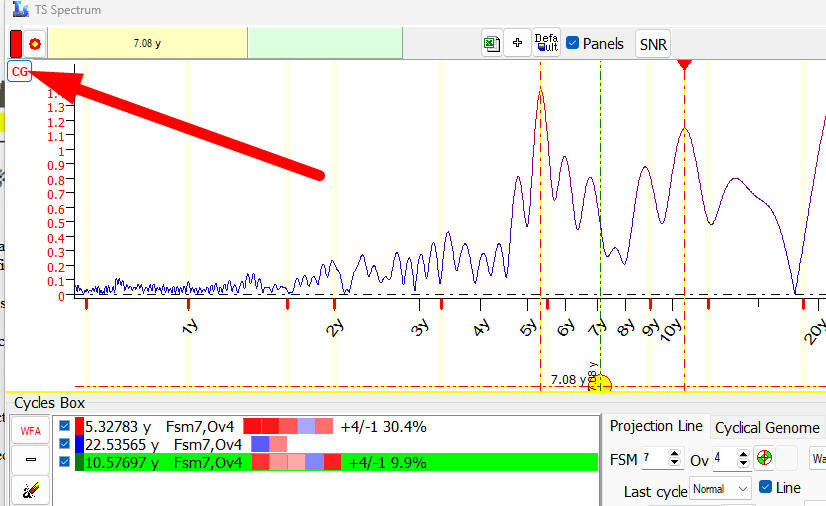

H-Spectrum module in

action

There are several ways to use

H-Spectrum module:

1) H-Spectrum for single

instrument (vary LBC only)

Firstly we can apply H-Spectrum for a single

financial instrument. Here is an example. I have downloaded Dow Jones

Industrial since 1885, opened TS Spectrum module and did this:

It takes 30 minutes to complete

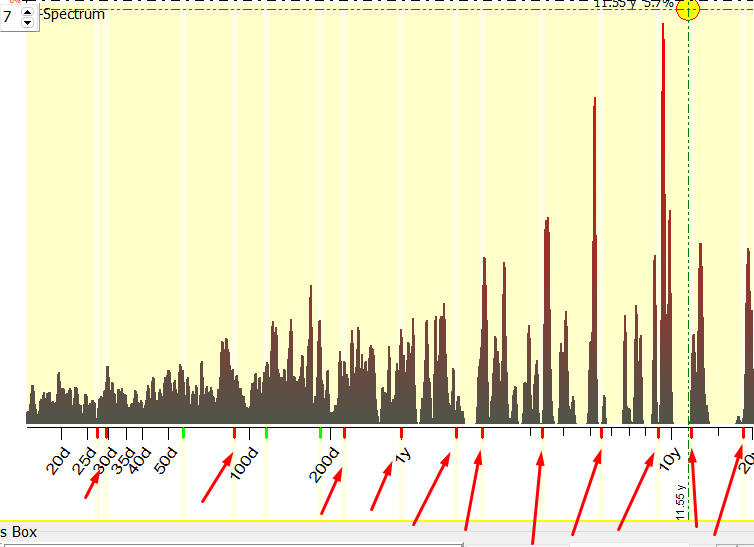

these calculations. As a final result we get H-Spectrum

for DJIA index. It shows the most typical cycles that appeared in DJIA chart

since 1948, i.e. we vary LBC position since 1948 till now (may

2024) and watch the cycles that appear within this period:

We analyze here temporary

cycles, i.e. cycles that live (i.e. can be observed within) some restricted

time only. This is why we need to move LBC position to see how historically

often these cycles appear.

The chart also shows that we

are "in the right direction": practically all the most important

cycles revealed by spectrum (they are marked by red arrows) have peaks on

H-Spectrum chart:

This tool is very good to confirm economical cycles. It is especially helpful

for financial data where the effect of heavy tailed statistic is very

important.

Briefly, this effect appears in

the situations when we see a peak on some periodogram calculated by classical

spectrum. That may be a result of some unusual price movement caused by some

extreme and rare event, or it could be a strong cycle that worked for a very

short period of time. The statistical significance of

this cycle is very low, i.e. with high probability we may consider it as some

occasional movement. Still, this peak on periodogram is very high, and we

should not ignore it. H-Spectrum algorithm is free of this problem.

2) Multiple financial

instruments (vary financial instruments and LBC)

The application of histograms

for cyclical analysis opens some new possibilities. We can calculate H-Spectrum

that gathers information from very different sources such as typical

periodograms for different American stocks calculated for different time periods.

Or another variation: we can calculate H-Spectrum that shows the recent

cyclical activity of American stocks based on 1000 American stock charts (this

is Cyclical Genome spectrum, available in Timing Solution; it will be explained

later). Classical Bartlett's method of averaged

periodograms does not allow to do that.

I would like to remind you

about this guy, Maurice Stevenson Bartlett:

Maurice Stevenson

Bartlett (1910 - 2002), English statistician

He studied and worked with many

great minds of the XX century. He made significant contributions to the

analysis of data with specific patterns contained. I have already mentioned

Bartlett/Welch method of averaged periodograms. It is the closest that I have

found to what we do here. However, this method does not allow to do things that

we can do with H-Spectrum. When calculating the averaged

periodogram, we drastically lose spectral resolution, especially on big

sample sizes. H-Spectrum works with extracted cycles, not with the periodogram

itself. This fact dramatically increases the resolution, especially on big

sample sizes. We can take H-Spectrum as an application of Maurice Stevenson

Bartlett ideas prolonged into the computer epoch when new computation

capabilities became available for researchers.

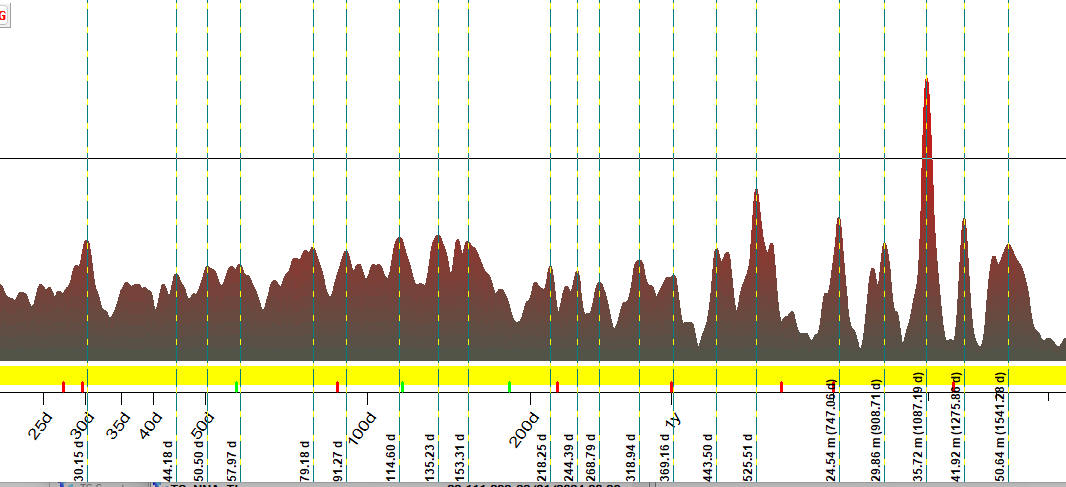

To calculate our first chart of

this article, the chart of cyclical activity for 12 American stocks since 2000

till now. - we have calculated periodograms for

these stocks varying LBC position since 2000 up to May 2024. In other words, we

vary here both - the analyzed American stocks and LBC positions. The resulting chart represents the

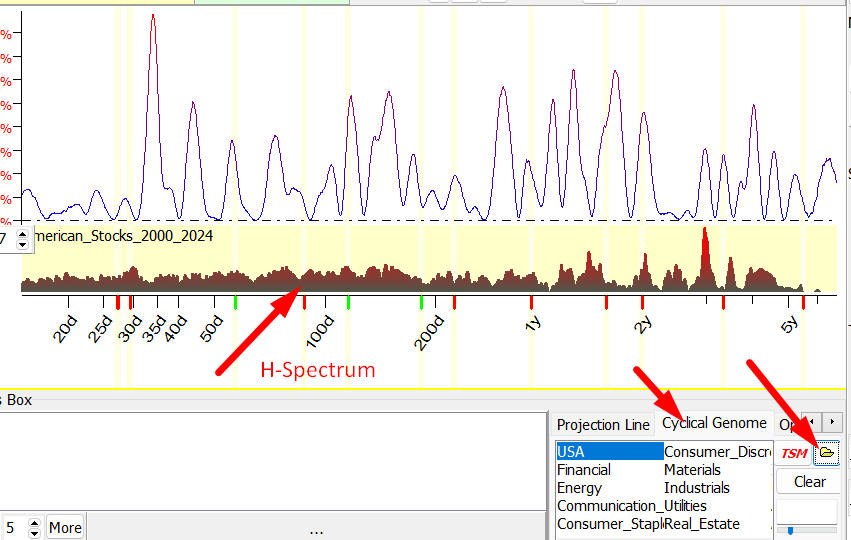

general cyclical picture for American stocks for the last 24 years.

As you can see, the most

important cycles here are 30.15 days, 44.18 days, 50.50 days, 57.97 days. and

so on; they are marked by vertical lines:

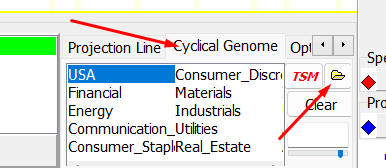

This H-Spectrum is available

for Timing Solution software users. It can be downloaded through TS Spectrum

module "Cyclical Genome" panel, by clicking this button and choosing

the file "Ameerican_Stocks_2000_2024.spectr":

BTW, I have not found any

certain confirmation that E.R. Dewey's cycles work. Dewey cycles are marked

here by vertical stripes:

It is possible that I have

incomplete information regarding Dewey's cycles. This issue requires more

research.

3) Cyclical Genome (vary

instruments only)

For traders' needs, this is the

most important feature. We do not play here with LBC. We use the latest price

history and conduct cyclical analysis for one and the same time

period. And we do that for as many stocks (or other financial

instruments of the same kind) as we want. In practice, this is what the program

does when we work with Cyclical Genome (CG): it

conducts cyclical analysis for some stock on a certain interval (the latest

price history is used). As a result, some cycle's presence is detected. Or

several cycles. Should we trust this cycle/cycles? Some additional confirmation

would be very helpful. In order to get this

confirmation, we keep calculating spectrums for hundreds and hundreds of

different stocks and watch if this cycle shows up in these stocks.

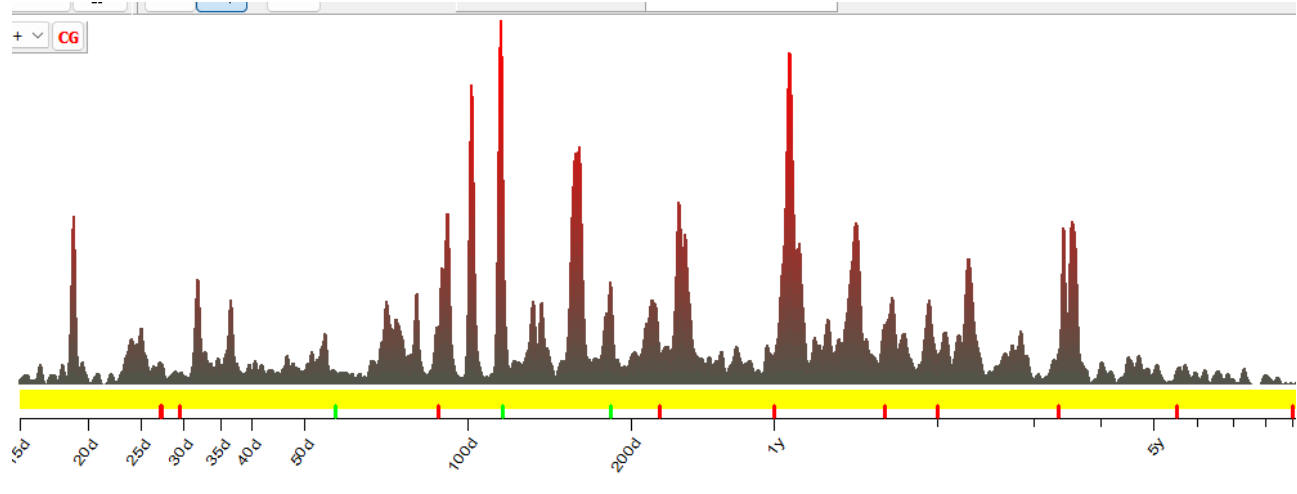

Look at the chart below. This

is Cyclical Genome (H-Spectrum) calculated for 1000 different American

stocks. It is created to reveal cycles that worked since March 2023(LBC set to March 2023):

We see here that some cycles

are present in the charts of many American stocks. It is not a surprise as the

companies operated in the USA are connected in many ways. If there is some

cyclical pattern for one company (found by calculating the spectrum for its

price chart), it may have some impact on other companies, the vendors or clients of the first one. This is the additional

confirmation regarding cycles that we need.

To calculate Cyclical Genomes

is an enormous computation task. That is why we perform these calculations

aside the software, on a specialized Timing Solution Server machine.

With the time, the cyclical

portrait of stocks is changing. Hence we need to

recalculate Cyclical Genome on a regular basis; we do that every other month.

This module can be qualified as a big data analysis system.

Instruction for Timing

Solution users

Working with H-Spectrum, please

remember the following.

Firstly, while you work with TS

Spectrum module, you can save a periodogram and extracted cycles by clicking on

this button (it saves this info into the file with the extension *,spectr):

This is the way to make your

own collection of periodograms, calculating them for different instruments

(stocks, etc.) and different time intervals.

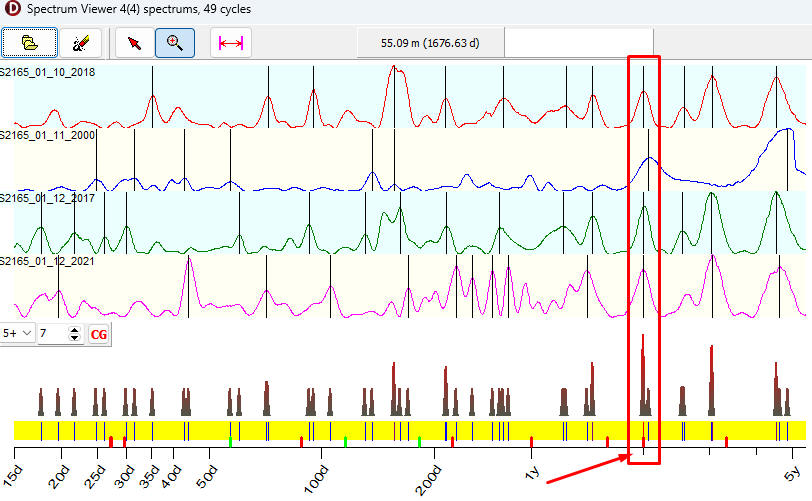

To work with these files, use a

special utility, Spectrum Viewer. You can run it through Miscellaneous

section:

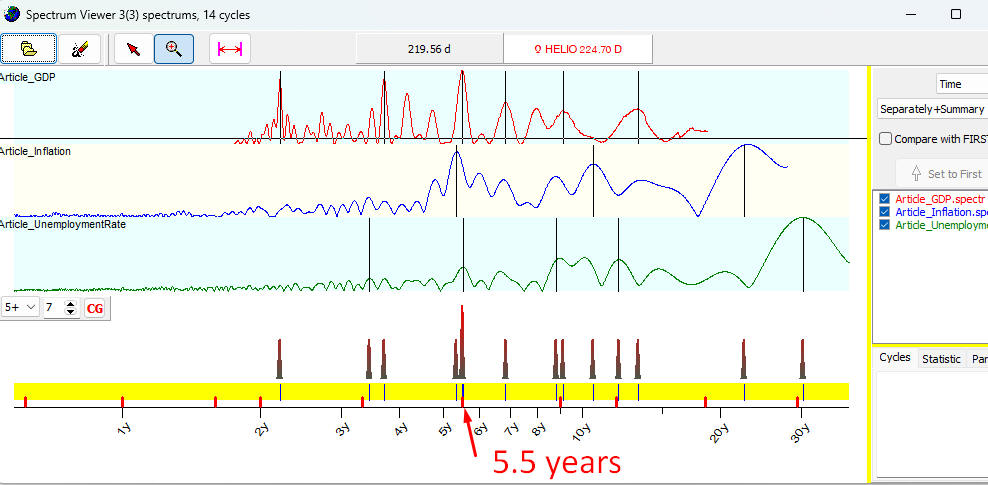

Here is an example of applying

this approach for three major economical indicators.

I have calculated periodograms

(using the algorithm that reveals permanent cycles) for GDP, CPI and

Unemployment rate and downloaded these periodograms into Spectrum Viewer:

As you see, the cycle with

period around 5.5 years works for all these indicators. H-Spectrum displays the

highest peak there.

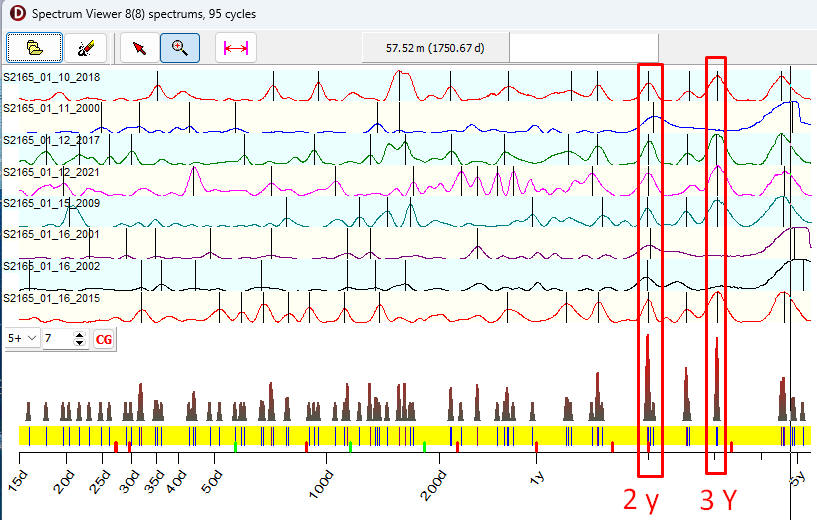

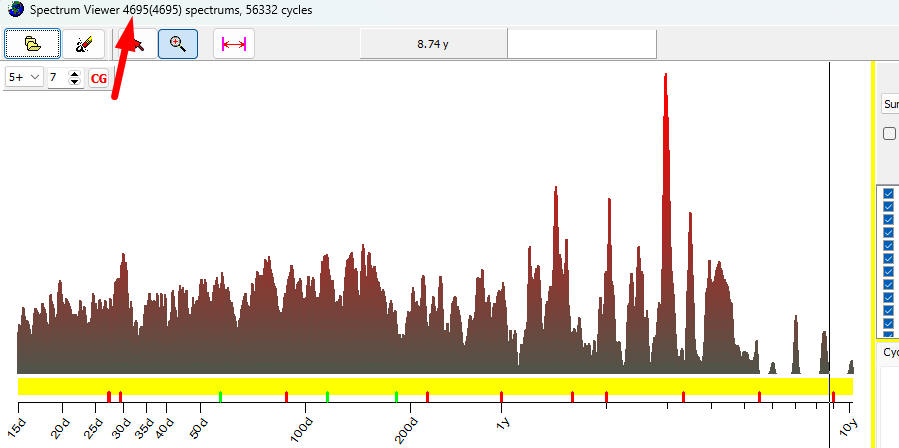

You can download into Spectrum

Viewer utility as many periodograms as you need.

For another example, I have

downloaded 4695 periodograms. The resulting histogram shows a distribution of

56332 revealed cycles:

You can save this H-Spectrum

into the file clicking this button:

After that, any time you want

you can display this H-Spectrum in TS-Spectrum module this way:

So you can see together the periodogram

calculated for your selected financial instrument and H-Spectrum that shows the

cyclical activity for the whole market.

May 28, 2024

Toronto, Canada